1 Introduction

Commercially contracted and sponsored clinical trials are those being managed and set up via pharmaceutical companies (for example, Sanofi, AstraZeneca, Novartis and Moderna) to explore the efficacy and safety of new medications (and in some cases technology) for delivery within the NHS setting. Often pharmaceutical companies will employ contract research organisations (CROs), for example, Parexel IQVIA, PPD, to manage aspects of the trial, including but not limited to: site identification, study set-up, contracting, budget negotiation and monitoring. Grounded Research within Rotherham Doncaster and South Humber (RDaSH) NHS Foundation Trust manage these relationships to ensure commercially contracted and sponsored clinical trials are appropriately and safely set-up and delivered and the costs are recovered. The National Institute for Health and Care Research (NIHR) is the arm of the Department of Health and Social Care (DHSC) that is responsible for research within the NHS in England. It therefore provides standardised templates and processes for the conduct of research, including clinical trials (both commercial and non-commercial) within the NHS.

2 Purpose

The purpose of this policy is to agree a set of principles for the distribution of income from commercially contracted and sponsored clinical trials.

The trust has responsibility to ensure there are appropriate financial governance arrangements in place for all commercially contracted clinical research studies that take place in the organisation. This includes ensuring that all trials are fully costed, the costs are recovered, and the income is distributed with maximum benefit to the Investigators, support services, care groups or corporate services, Grounded Research and trust to incentivise research teams and grow research capacity.

This paper sets out the proposed principles for the distribution of income to where costs are incurred in the first instance and to ensure care groups or corporate services, support services, Grounded Research and Investigators are incentivised fairly through the distribution of surpluses and capacity building overheads, generated from commercially sponsored clinical trials (not academically or NHS sponsored, or industry partnered projects).

Several contributing factors have resulted in the need to review the current distribution of income from commercially contracted clinical research studies. The principles which underpin this includes:

- the adoption nationally of the National Institute for Health and Care Research or NHS England national contract value review (NCVR) and associated interactive costing tool (iCT) for all commercial studies, including those which are non-National Institute for Health and Care Research portfolio adopted, has resulted in an improvement to the transparency of costs included in the study

- departments and individuals are recognised and incentivised for their contribution

- all relevant costs incurred are recovered from the Commercial Sponsor

- commercial research affords opportunities to fund additional research or research related activities

- income from commercial research can be distributed and carried over in line with the finance control procedures of individual NHS organisations

- involvement of the Regional Research Delivery Network (RRRN) in NHS organisations research planning

- overly onerous itemisation and invoicing of study costs are avoided where possible

3 Scope

This document applies to and is relevant across all commercially contracted clinical research hosted by the trust, undertaken by trust staff within Grounded Research or within all care groups, or individuals appointed on honorary contracts, who are incurring costs for the trust or utilising trust resources.

4 Responsibilities, accountabilities and duties

The Grounded Research Senior Management team and Governance team will work with sponsors to ensure timely provision of the interactive costing tool to relevant study teams, care group research and innovation representatives (where relevant) and the finance team to ensure the principles outlined in this policy can be applied on a case-by-case basis as projects enter the set-up period. Throughout the lifecycle of a commercially sponsored clinical trial this group of people will meet quarterly to ensure the mechanisms in place to receive, manage and allocate the income within the care group or within Grounded Research are working appropriately and that the process is transparent and fair.

5 Procedure

5.1 The interactive costing tool

As part of the NHS England Standard Contract with NHS providers, the national directive on commercial contract research studies sets out the requirements providers need to adhere to for commercial contract research, which includes the mandated use of the standard costing methodology (the National Institute for Health and Care Research interactive costing tool) from 1 October 2018. Since its launch, the interactive costing tool has provided companies and NHS organisations with a single consistent approach to calculating commercial trial costs which is both clear and transparent for negotiating and establishing a price for research within the NHS.

The income distribution model described in this document is based on the National Institute for Health and Care Research interactive costing tool cost methodology to support the redistribution of commercial contract income for National Institute for Health and Care research portfolio studies.

The web-based interactive costing tool (iCT) provides a clear standard methodology to calculate consistent and transparent prices for the resource associated with delivering each commercial contract study to support the both the life-sciences industry and the NHS to help minimise set-up time related to cost agreement.

The methodology identifies Agenda for Change (AfC) rates for specific bands of NHS staff time representing the direct costs. Any indirect costs (including overheads) are covered by the indirect cost and capacity building elements. Prices for investigations and costs for departments supporting research are also included. These values are all localised with the national tariff market force’s factor (MFF) for the NHS organisation in which the research takes place (see appendix A). This document outlines good practice for appropriate funding flow of these elements to participating directorates and supports the establishment of suitable local arrangements.

5.2 Direct costs, NHS staff time

National hourly rates are calculated for the agreed NHS staff bands using the highest salary in the relevant Agenda for Change band which are adjusted to incorporate the NHS employer contributions for National Insurance and pension. This is a standardised representation of the direct cost to an employing NHS organisation and is used to calculate the template values for all procedures or tasks that are related to staff time.

Ideally these direct costs should be reimbursed to the care group, corporate service or directorate where the staff member is employed to compensate for the work performed.

For commercial studies involving university staff, an agreement should be in place between the relevant NHS organisation and university to agree suitable distribution of the NHS staff time costs or the mechanism to be applied to accommodate alternative cost approaches, for example, application of full economic costing (FEC), based on the National Institute for Health and Care Research interactive costing tool.

5.3 Indirect costs (overheads)

A standard rate of 70%, added only to the NHS staff time direct costs, provides a representative value for the indirect costs when conducting a commercial trial which are not already covered by the direct costs (that is, the real cost of carrying out a research activity). These indirect costs include physical aspects such as heating, lighting, building maintenance, and security; as well as the support functions required to deliver a clinical trial such as finance, general administration, human resources, information systems and corporate management (for example, corporate oversight offered by the chief executive officer, the director of finance, research and innovation director and others to ensure efficiency and cost savings within the organisation). This includes the corporate responsibility to drive research and find efficiencies to incentivise the individuals and services involved in delivering research. This element has a direct impact on the sustainability of the research activity and the research environment as a whole.

5.4 Capacity building

A capacity building rate of 20%, which is added to both direct staff time costs and investigations, should be considered as a “system optimisation” which is designed to build sustainable research and innovation capacity to the benefit of all research partners. The successful utilisation of this element requires significant commitment and resources from all research partners.

This element is separate from the 70% indirect costs to enable it to be easily ring-fenced for maintaining, strengthening, and adapting and growing sustainable research capacity over the long-term. It is supported by the Health Service Guidelines (HSG) 97-32 “Responsibilities for meeting patient care costs associated with research and development in the NHS”, which acknowledges that NHS income derived from commercial contract studies is raised through NHS income generation powers for “improving the health service”.

5.5 Market forces factor (MFF)

NHS England publish a market forces factor tariff which provides an adjustment value to accommodate the unavoidable cost differences of providing healthcare across the country. In the interactive costing tool it is applied to localise the national rates for the location in which the research is being conducted.

For funding flow, this factor should be applied to each element of the cost methodology to provide a true reflection of the cost for that location (for example, NHS staff time including market forces factor; indirect costs including market forces factor; and capacity building including market forces factor). Ideally, this should not be treated as a separate element but an integral part of each cost complement.

5.6 Per patient costs (including additional itemised costs)

The “per patient budget” and the “additional itemised cost” sections (the latter being where trial related costs that may not directly correlate with patient numbers or visits are included) applies all these aspects to two different cost calculations:

- Procedure costs = NHS staff time (direct costs) + 70% indirect costs + 20% capacity building + market forces factor

- Investigation costs = NHS direct costs for investigations + 20% capacity building + market forces factor

Note that NHS direct costs for investigations are already inclusive of the NHS organisation’s indirect costs and operating overhead.

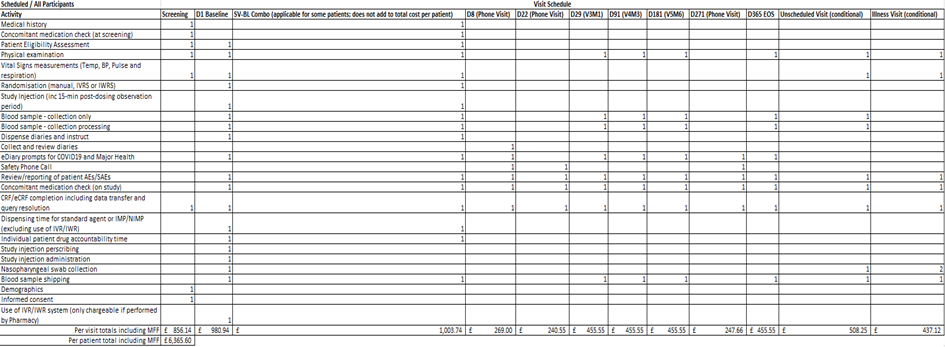

To illustrate the impact in applying the overhead, capacity and market forces factor charges onto the direct costs of performing the commercial research activity, figure 1 represents the National Institute for Health and Care Research interactive costing tool on the central portfolio management system (CPMS) for a recent commercial study at the trust. The total per participant budget is £3,348.50 (excluding any unscheduled visits or activity). Whereas figure 2 represents the final agreed budget in the contract (also known as the model clinical trial agreement (mCTA)) with the sponsor organisation, and once the overhead, capacity charge and market forces factor are applied the per participant budget is almost double at £6,365.

5.7 Set-up and other trial related costs

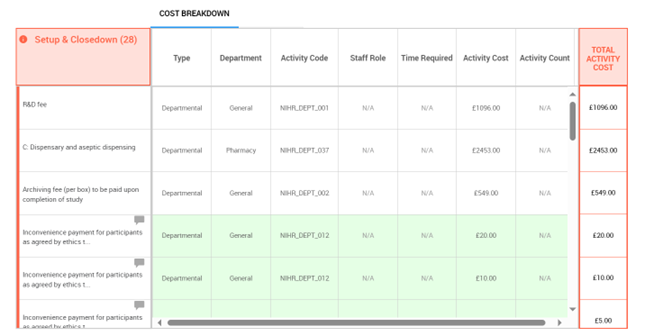

The pre-trial and ongoing related study costs are managed through the use of set-up, management and close down fees and separate costs which are assigned to the relevant department. The interactive costing tool uses recommended fees based on national averages to provide a list of potentially applicable fees depending on the study requirements (as shown in figure 3 below).

5.8 Distribution of the 70% indirect cost element

The wide reach of tasks covered by the 70% indirect costs component supports the splitting of this value to enable representative, but practical distribution to the relevant parties involved in delivering the commercial research.

The National Institute for Health and Care Research income distribution model recommended has been adjusted to local requirements to ensure:

- that it’s the corporate body and not the individual that is in receipt of this income, with the individual incentivisation and discussion occurring within care groups or corporate services

- that the research and innovation group are the decision-making body for these principles

- that the finance and contracting teams have the capacity and capability to manage this process of distribution of income

Note, the distribution split of the indirect cost element assumes that all direct staff costs and the cost of investigations are paid direct to the NHS organisation as per the arrangements of the relevant model clinical agreement and where these costs are incurred by support departments or external providers; the costs are paid or passed through as per local agreement.

5.9 Distribution of the 20% capacity building element

The intended use of the capacity building element within the NHS organisation should be clearly documented to support and evidence its reinvestment in research in line with the overarching intention to “improve the health service”.

It is best practice for NHS organisations to have some form of expenditure plan for the capacity building element with supporting accounting processes to manage and evidence the distribution. This could be incorporated into existing reports or plans to minimise duplication. For example, the expenditure plan may include:

- an aggregate expenditure for large-scale, long-term resource and infrastructure projects (for example, funding additional staff posts, building resource in research constrained departments or services)

- small-scale department or unit specific plans as part of an open local competition or application process (for example, development of training programmes, part funding of department specific research posts, “buying-out” or reserving “blocks” of research time in departments and units)

- a mixture of both

5.10 Control of the funds

An income distribution model is most effective when all income values are transparent to all directorates involved through good local accounting allocations, clear distribution rule application and central NHS organisation oversight (for example, by the Grounded Research and Finance teams). While income is distributed back to individual directorates to support engagement in commercial research, the use of this income should be managed and monitored through spending plans which are reviewed and approved centrally by the NHS organisation. This approach ensures an integrated approach to research development across the NHS organisation.

5.11 Carryover of funds

Local agreements should be used to manage the carryover of funds generated from commercial contract research, which may be key to raising the profile of research within the NHS organisation. In the case at the trust these funds can be deferred to be utilised in future financial years, as part of the Grounded Research budget (deferred income budget line) or via the set-up of care group specific deferred budget lines.

5.12 Trust proposed commercial income distribution

| Income category | Care group or corporate service | Grounded Research | Central or deferred income |

|---|---|---|---|

| Direct costs | 0% | 100% | 0% |

| Overhead | 0% | 90% | 10% |

| Capacity | 0% | 100% | 0% |

| Market forces factor (MFF) | 0% | 0% | 100% |

| Income category | Care group or corporate service | Grounded Research | Central or deferred income |

|---|---|---|---|

| Direct costs | 100% | 0% | 0% |

| Overhead | 50% | 40% | 10% |

| Capacity | 100% | 0% | 0% |

| Market forces factor (MFF) | 0% | 0% | 100% |

100% of direct costs for staff to be directed to where the costs incurred for the salary, for example, within care groups or Grounded Research)

Any surplus income above salary costs incurred within Grounded Research to be deposited in deferred income.

10% of overhead charge is negotiable on a case-by-case basis dependent on support from central or corporate teams

If there is a mixed model of workforce support across Grounded Research and care groups or corporate services the relevant scenario for each workforce should be applied, for example, principal investigator based in Grounded Research but nurse or allied health professional and admin time in care groups or corporate services.

5.13 Pharmacy Costs

5.13.1 Staff time

Staff time hourly rates distributed to the department where the staff member is employed to cover the cost of their involvement in the research.

5.13.2 70% indirect costs

Collected and collated for allocation to the NHS organisation pharmacy for indirect cost coverage, that is, the real costs of conducting research within the pharmacy.

5.13.3 20% capacity building

Collected, collated and reinvested by the NHS organisation to build sustainable research and innovation capacity to the benefit of all research partners.

5.14 Set-up, management and close-down costs

5.14.1 Department or task fee

Template value: Distributed to the department where the set-up task was performed or costs incurred, for example, research and innovation, service support department, clinical research facility, care group or corporate services to cover the cost of their involvement in the research.

6 Training implications

There are no specific training needs in relation to this policy, but the following staff will need to be familiar with its contents: Senior Management team and Governance team in Grounded Research (GR), any principal investigators or sub-investigators on commercially sponsored clinical trials (whether located in Grounded Research or within a care group), care group research and innovation representatives, finance colleagues involved in either research or with care groups where commercially sponsored trials are taking place, chief pharmacist (and deputy) and any other individual or group with a responsibility for implementing the contents of this policy.

As a trust policy, all staff need to be aware of the key points that the policy covers. Staff can be made aware through a variety of means such as:

- research and innovation group dissemination

- research and Innovation panel dissemination

- supervision

- care group research meetings

- team meetings

7 Monitoring arrangements

7.1 Income distribution model on a case-by-case basis as commercially sponsored clinical trials are set up and delivered across the organisation

- How: Regular care group meetings.

- Who by: Care group research and innovation representatives, principal investigator, finance and Grounded Research team.

- Reported to: Director of finance and estates.

- Frequency: Quarterly.

8 Equality impact assessment screening

To access the equality impact assessment for this policy, please email rdash.equalityanddiversity@nhs.net to request the document.

8.1 Privacy, dignity and respect

The NHS Constitution states that all patients should feel that their privacy and dignity are respected while they are in hospital. High Quality Care for All (2008), Lord Darzi’s review of the NHS, identifies the need to organise care around the individual, “not just clinically but in terms of dignity and respect”.

As a consequence the trust is required to articulate its intent to deliver care with privacy and dignity that treats all service users with respect. Therefore, all procedural documents will be considered, if relevant, to reflect the requirement to treat everyone with privacy, dignity and respect, (when appropriate this should also include how same sex accommodation is provided).

8.1.1 How this will be met

No issues have been identified in relation to this policy.

8.2 Mental Capacity Act (2005)

Central to any aspect of care delivered to adults and young people aged 16 years or over will be the consideration of the individuals’ capacity to participate in the decision-making process. Consequently, no intervention should be carried out without either the individual’s informed consent, or the powers included in a legal framework, or by order of the court.

Therefore, the trust is required to make sure that all staff working with individuals who use our service are familiar with the provisions within the Mental Capacity Act (2005). For this reason all procedural documents will be considered, if relevant to reflect the provisions of the Mental Capacity Act (2005) to ensure that the rights of individual are protected and they are supported to make their own decisions where possible and that any decisions made on their behalf when they lack capacity are made in their best interests and least restrictive of their rights and freedoms.

8.2.1 How this will be met

All individuals involved in the implementation of this policy should do so in accordance with the guiding principles of the Mental Capacity Act (2005).

9 References

- National Institute for Health and Care Research guidance for the distribution of income from commercially sponsored clinical trials

- National Institute for Health and Care Research guidance on utilization of the interactive costing template

- The National Institute for Health and Care Research or NHS England National Contract Value Review

10 Links to any other associated documents

If any volunteers, patient research ambassadors (PRAs), Community Contributors and, or people with lived experience are involved in the promotion of commercially sponsored clinical trials then their time will be reimbursed as per the patient research ambassador and community contributor local working instruction (staff access only).

11 Appendices

11.1 Appendix A 2025 to 2026 tariff prices for the interactive costing tool

Learn how the interactive costing tool (iCT) calculates the costs of studies at sites.

11.2 Appendix B National Contract Value Review (NCVR) presentation to Research and Innovation Panel

Refer to appendix B: National Contract Value Review (NCVR) presentation to Research and Innovation Panel (staff access only).

11.3 Appendix C definitions

| Term | Definition |

|---|---|

| Commercial | There are studies which are generally sponsored and funded via a commercial company, usually a pharma company. There may be investigator led studies which are funded via the company but sponsored at the trust or other trust or university. The interactive costing tool (iCT) is used to determine the costs of commercial studies, if managed on the portfolio. |

| Central portfolio management system (CPMS) | Holds the National Institute for Health and Care Research clinical research network (CRN) portfolio. Central portfolio management system is used by the clinical research network to support study management. It is also used by commercial partners to submit clinical research network service requests and is the portal through which the interactive costing tool can be accessed. |

| Deferred income | Deferred income budget references the portion of the budget which can be ‘carried over’ into future financial years. Only commercial income should be used in this way. Currently the National Institute for Health and Care Research grants that run across multiple years, and underspent funds may be placed in deferred income and then moved back to the project account in the new financial year. |

| Interactive costing tool (iCT) | An interactive costing tool facilitates faster and consistent costing and contracting between commercial sponsors and NHS sites. |

| National Institute for Health and Care research (NIHR) | The National Institute for Health and Care research is funded by the department of Health and Social Care, focusses early translation research, clinical research and applied health and social care research. Working in partnership with the NHS, universities, local government, other research funders, patients and the public, they fund, enable and deliver world leading health and social care research that improves people’s health and wellbeing and promotes economic growth. |

Document control

- Version: 1.

- Unique reference number: 1106.

- Approved by: Finance group.

- Date approved: 8 April 2025.

- Name of originator or author: Deputy director of research and innovation.

- Name of responsible individual: Chief medical officer.

- Date issued: 23 May 2025.

- Review date: 31 May 2028.

Page last reviewed: June 20, 2025

Next review due: June 20, 2026

Problem with this page?

Please tell us about any problems you have found with this web page.

Report a problem